Benefits and costs of risk insurance in selected countries of Asia

Keywords

Agriculture · Benefits · Climate change adaptation · Costs · Disaster risk reduction · Risk insurance

Highlights

- The benefit-cost ratios (BCR) of risk insurance were largely positive but varied across the countries.

- Profitability of insurance in terms of BCR ratios differ from country to country. The benefit-cost ratio was found to be 2 in India and 1.5 in the Philippines; it was highest in Malaysia (9.6).

- The BCR ratios also change depending on the frequency of disasters. For example, in the Philippines, where disasters occur annually, crop production without crop insurance can be possible. However, having insurance increases the BCR ratio further. Hence, availing of crop insurance will increase the financial profitability of crop production.

1. Introduction

The Asia-Pacific region is one of the most vulnerable regions to a range of primary hydro-meteorological hazards such as storms, floods and droughts. In the Asia-Pacific region, hydro-meteorological disasters claimed the lives of 0.22 million people with estimated total economic damage costs of US$ 285 million during 2001–2012 (Prabhakar et al., 2013). An increase in the number of catastrophic disasters and related insured and uninsured losses has been reported. These disasters are undermining the developmental gains across the Asia-Pacific region and indeed the world. In this context of high vulnerability, insurance has been suggested as an important risk management tool at all levels as it promotes emphasis on risk mitigation compared to response, provides a cost-effective way of coping with the financial impacts, supports climate change adaptation by covering the residual risks not covered by other risk reduction mechanisms, stabilizes rural incomes, provides opportunities for public-private partnerships, reduces the burden on government resources for post-disaster relief and reconstruction, and helps communities to renew and restore their livelihoods (Prabhakar et al., 2015).

Though there are several policy and institutional initiatives to promote insurance in the Asia-Pacific region, the region has not been able to utilize the full potential of insurance. The problems facing insurance include poor internalization of insurance benefits, high insurance costs, poor access and availability of weather data, poor risk mitigation, lack of enabling policies, imperfect information, and technical complexity. A deeper problem is the lack of clear assessment and understanding of insurance benefits and costs in terms of disaster risk reduction, climate change adaptation and sustainable development among the stakeholders engaged in insurance policy-making and delivery.

Part of the problem also lies with the traditional understanding of insurance effectiveness that revolves around the delivery of contractual obligations, i.e. payouts as agreed in the contract. Insurance effectiveness is thus mainly assessed based on the number of people insured, avoidance of moral hazards and adverse selection, as well as minimization of basis risk. However, these indicators provide an inadequate and even misleading understanding of insurance effectiveness in the context of climate change adaptation and disaster risk reduction. Traditionally, the insured are often not required to invest payouts in better risk mitigation practices. As a result, every disaster and the resulting payouts can perpetuate the risk. From this basic observation, it is clear that the assessment of insurance effectiveness in the contexts of DRR and CCA requires consideration of appropriate indicators. There is a need to change from a cycle of risk perpetuation to a cycle of risk reduction.

In order for insurance to make a real difference in terms of risk reduction, there is a need to understand the benefits and costs associated with risk insurance so that the insurance can be designed to enhance the benefits while keeping the costs low. Keeping this in view, this project has conducted case studies to assess the benefits and costs associated with risk insurance in India, Philippines and Malaysia using structured household surveys.

1.1 Costs and benefits of insurance

Insurance can provide several costs and benefits both to the subscriber and to society as a whole at a macro level. Table 1 lists several costs and benefits associated with insurance as reported in the literature. These benefits and costs can be grouped into social and economic costs and benefits. Costs can be both direct and indirect. Direct costs are easy to assess as they are visible to the one who is paying them. However, indirect costs are difficult to assess and can lead to subjective conclusions if they are not properly defined and the association is well established, hence the reason why very few indirect costs were identified in the published literature and in Table 1. The same can be said for both direct benefits and indirect benefits. The published studies indicated that household incomes could be stressed if insurance premiums are high, sometimes even leading to borrowing to pay premiums, and could lead to fortified profits due to alternated investments. Uncompensated losses could result if insurance losses were not satisfactorily assessed and delayed payments could have compounding impacts on the insured that may not be undone by the payouts received after the delay.

In terms of benefits, insurance could result in consumption smoothing, i.e. less difference in consumption between a good year and a disaster year, reduced debt and improved creditworthiness over the years. More indirect benefits were reported than indirect costs indicating possible overall benefits associated with insurance. However, insurance could lead to instances where the insured may indulge in risk-seeking behaviour resulting in adverse selections that could stress the insurance market and insurance providers.

| Category | Costs | Benefits | ||||||

| Justification | Costs | Source | Justification | Benefits | Source | |||

| Social | Income stress due to high premium cost. Difficulty in paying premium. | Direct | Indirect | Mechler et al., 2008 | Consumption smoothing

No income fluctuation |

Direct | Indirect | Rosenzweig, and Wolpin, 1993; |

| Increased loans taken for premium payment. | Reduced consumption. | Steady income in loss month | Reduced Debts

Preserved assets Increased Investment expenditure |

|||||

| Opportunity costs insurance premium | Forfeited profits from alternated investments | Mechler et al., 2008 | Improved creditworthiness

Increased opportunity for increasing livelihood profitability |

Increased bank loans taken for high yield crop/farm practices (machinery investments etc.) | Increased farm profits | Hazell et al.,1986; Mishra, 1994 | ||

| Economic | Basic risk, losses from un-covered

Risks |

Uncompensated crop losses, payout does not reflect losses | Clark et al., 2012; Merchler et al., 2008; Gosh and Yadav, 2008 | Increased confidence, post-disaster liquidity, ability to recover from disaster | Increased high risk high yield variety crops planted, increased monoculture, increased investment in livelihood assets, funds available for post-disaster investments for livelihood and rebuilding | Increased profits, preserved assets, reduced debts | Hazell, 1992; Venkatesh, 2008 | |

2. Methodology

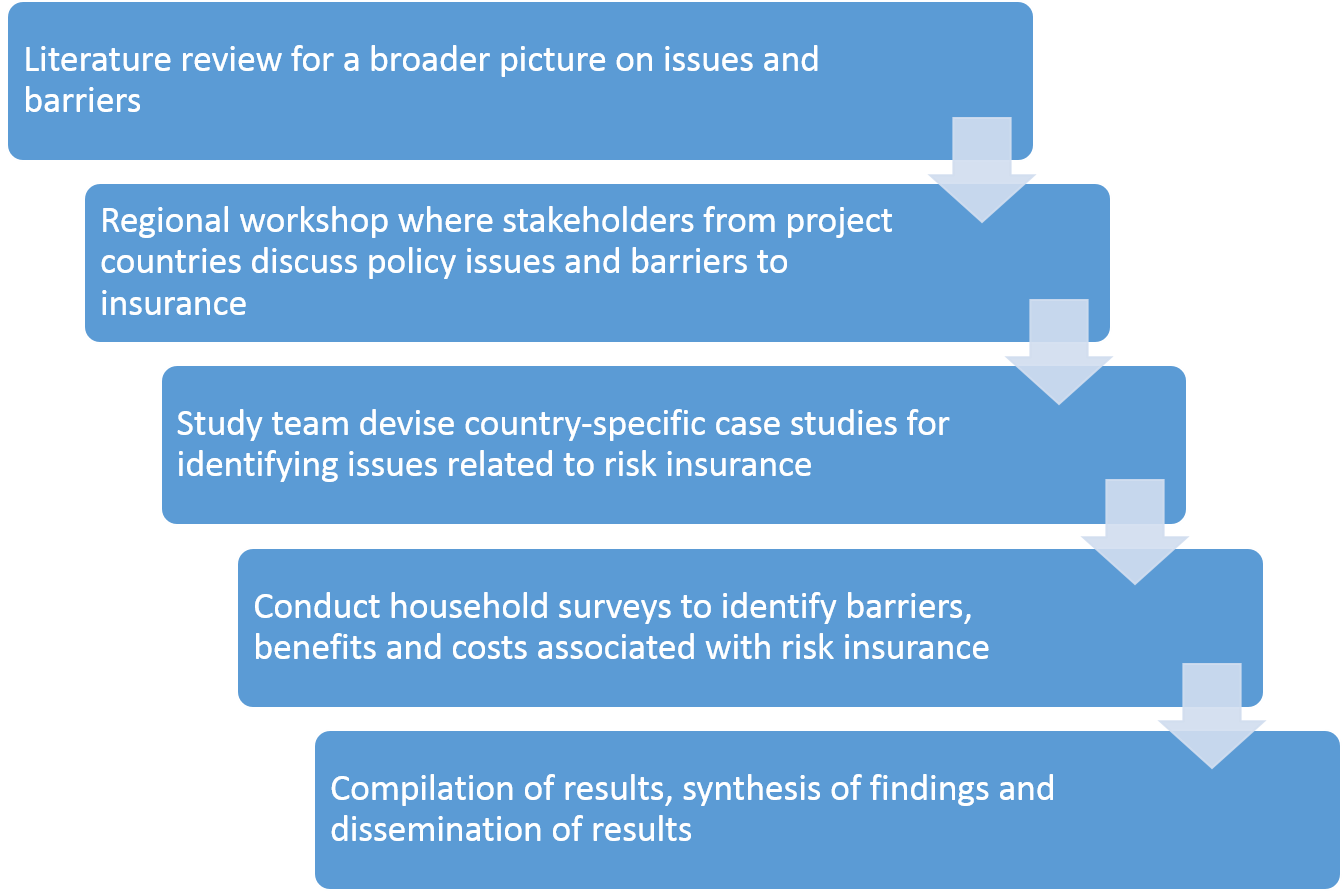

The project team has devised a multi-country case study-based methodology that looks into country-specific circumstances of risk insurance and assesses the benefits and costs of risk insurance and stakeholder perspectives (Figure 1).

2.1 Insurance background in the case study countries

Both India and the Philippines have a long history of risk insurance in the form of agricultural insurance. Agricultural insurance products in both countries have undergone significant changes over the years through continuous efforts to fine-tune the insurance delivery mechanisms and by delivering multiple insurance products targeting various sub-sector requirements. For the purpose of the study, paddy crop insurance was chosen in these two countries. In India, the insurance was weather index insurance linked to the crop loan, while in the Philippines it was indemnity-based insurance offered by the Philippine Crop Insurance Corporation. Plantation insurance is prominent in Malaysia. However, access to the plantation owners was not possible due to limited access to these stakeholders by the study team. Hence, homestead insurance for floods was chosen for assessing the benefits and costs associated with insurance.

2.2 Household surveys

Household and stakeholder surveys were carried out in three countries to assess stakeholder perspectives and benefits, and costs associated with the risk insurance. For this purpose, agriculture insurance was chosen as a form of insurance that is targeted at the predominant livelihood of the people in the project countries except in Malaysia where homestead insurance was considered due to lack of an active agriculture insurance in the country. Household surveys and consultations were conducted using a multi-method approach consisting of focus group discussions, structured questionnaire surveys, and small farmer group workshops.

Detailed structured questionnaire surveys were implemented at the community level to understand needs and perception issues to be considered for formulating effective insurance programmes and to understand benefits and costs associated with risk insurance at the local level. The structured questionnaires consisted of questions on the demographic background of the respondent, the past crop loss experience, opinion on the insurance currently enrolled (in case of insured) and on available insurance options (in case of non-insured and in Malaysia where there is no crop insurance in place). A generic questionnaire developed commonly for all the countries was further modified before implementing the survey by the respective country partners taking into consideration the individual country contexts such as type of insurance product being offered. The sample size was determined based on the resources at hand rather than the size determined based on the statistical sampling. However, households were selected randomly based on the stratified random sampling procedure. The elicited responses were analyzed for specific preferences among communities for certain form of risk reduction based on self-evaluation of their experience in crop insurance and presented as a percentage of responses.

2.3 Benefit-cost analysis

Benefit-cost analysis (BCA) is a major decision support tool that is used by stakeholders to organize and understand the socio-economic benefits and costs and inherent trade-offs of decisions made (Mechler, 2016). BCA has come to the forefront notably for the appraisal of efficiency of disaster management projects, development projects and public interventions (Mechler, 2005). Overall, BCA can provide valuable information that goes beyond the rhetoric and help in the selection of contextual and best-suited interventions. BCA was used to identify the impacts of crop insurance on households, classifying these impacts into benefits and costs, and identifying and quantifying the economically-relevant impacts. The benefit-cost ratio was calculated using the following generic formula (Equation 1).

Benefit-cost ratio =  Equation 1

Equation 1

Only direct benefits and direct costs were considered in all the countries. Direct costs included the price of the premium paid and direct benefits included the insurance payout received after the insurance was triggered. Moral hazard was calculated as an amount of insurance payout that was used for other than replacing or repairing the damaged property such as crop field or house. Transaction costs were not separately considered since the premium price is taken as a whole unit. No transaction costs were considered from the buyer side. The indicators for benefits and costs were developed using literature review and experts’ opinions (Figure 1) and the identified indicators were used in the development of questionnaires.

Detailed structured questionnaire surveys were implemented at the community level to understand needs and perception issues to be considered for formulating effective insurance programmes and to understand benefits and costs associated with risk insurance at the local level. The structured questionnaires consisted of questions on the demographic background of the respondent, the past crop loss experience, opinion on the insurance currently enrolled (in case of insured) and on available insurance options (in case of non-insured and in Malaysia where there is no crop insurance in place). A generic questionnaire developed commonly for all the countries was further modified before implementing the survey by the respective country partners taking into consideration the individual country contexts such as type of insurance product being offered. The sample size was determined based on the resources at hand rather than the size determined based on the statistical sampling. However, households were selected randomly based on the stratified random sampling procedure. The elicited responses were analyzed for specific preferences among communities for certain form of risk reduction based on self-evaluation of their experience in crop insurance and presented as a percentage of responses.

2.4 Study locations

In India, the study was conducted in the Khammam and Warangal districts in Telangana. Fifty eight households were surveyed to assess the benefits and costs associated with agricultural insurance. The surveys were conducted in two villages, Perumala Sankeesa and Rajolu. In Malaysia, the data was collected from 30 households through structured questionnaire surveys. In Malaysia, the respondents were householders in Kemaman, a district in Terengganu. In the Philippines, the data was collected through a household survey of farmers in the municipalities of Sta. Cruz and Sta. Maria, in the Province of Laguna, involving 563 farmers. These surveys were complemented with focus group discussions (FGDs), field observations and photo documentation. Due to the limited sample size, the associated results should not be construed for their representation to the study locations but only those of the respondents who participated in the study.

3. Results and Discussion

In this section, results from the three case study countries are presented. Overall, it can be observed that insurance has helped households to cover part of the losses associated with a disaster. Subsidizing of premiums have played a significant role in improving the access and acceptability of insurance. However, instances were observed where the premium levels paid by the insured and the payouts received after the insurance triggered varied significantly. Such discrepancies may have led to lack of trust on the insurance providers and the loss estimation procedures employed. Overall, the insurance has provided a positive BCR for the insured in all the case study countries.

3.1. India

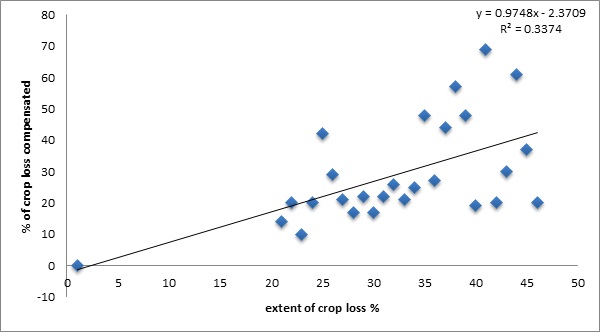

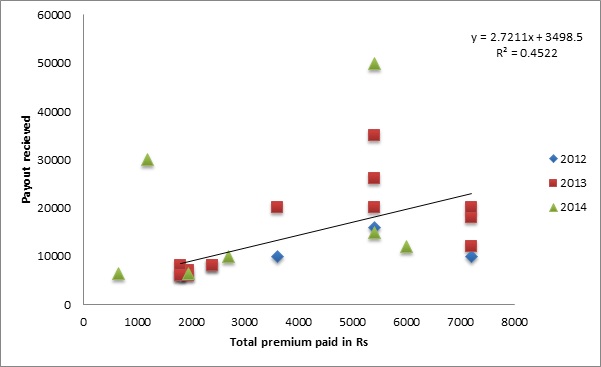

The study indicated that uninsured farmers prefer to invest money for the purchase of livestock (46% among insured compared to 17% of insured farmers) and more insured farmers (28%) have made significant investments, particularly in small business compared to uninsured farmers. Furthermore, only 10% of insured farmers felt that there was even a moderate potential for implementing alternate strategies to insurance. A significant downside of crop insurance is the potential lack of correlation between payment and actual losses (Figure 2). The survey revealed a correlation coefficient of 0.2 between the percentage of crop loss covered by the insurance payout to premium paid in loss years 2012, 2013 and 2014. This low level of correlation indicates that the premium does not reflect the payment for losses. Similarly, comparing the percentage of crop loss to the percentage of crop loss that was compensated by the insurance the correlation is only 0.14, indicating that the level of correlation between the actual loss and compensation received is quite low (Figure 3).

Eighty five percent of insured farmers reported making household consumption adjustments during the last season of crop loss. This was higher than 75% of uninsured farmers who made household consumption adjustments during the same period. This indicates that insurance has not had a significant impact on household income fluctuations and in effect the need for consumption adjustments during periods of crop loss. The plausible explanation for this could be that the smaller farmers who are not enrolled in insurance are highly subjected to consumption adjustments while the farmers who could afford insurance are not.

The survey showed that in the previous crop loss year, 64% of uninsured farmers sold assets to cover losses compared to 36% of insured farmers. Forty three percent of uninsured farmers reported selling livestock during the loss season; of these farmers, 50% reported that they had to sell their cattle below market price. This suggests that insurance has reduced the need for farmers to sell assets to cover losses. For the same loss year, 64.2% of uninsured farmers reported taking loans to cover crop losses, 39% of farmers reported that they took these loans from banks as well as money lenders, and 53% of farmers reported that they had partially repaid the loan. The prominent reason for taking the loan was unexpected household expenses (46.4%). Eighty two percent of insured farmers reported that they took loans during the season they suffered crop loss; of these farmers, 74% of insured farmers reported that they borrowed money from money lenders.

Farmers perceived that the biggest cost of insurance was the income stress caused from paying premiums (42.8%). This is reflected in the majority of farmers’ opinion that the premium should be completely subsidized by the government (67.8%). Unavailability of cash during crucial periods was also identified as a cost of insurance; the average time between claims and payout was 7 months. Consumption smoothing was perceived to be the biggest benefit of agricultural insurance (64.2%) and this is followed by an increase in confidence (57.14%) and ability to recover from disasters (42.8%). Based on the assessment of benefits and costs of agricultural insurance, the benefits and costs that can be monetarily quantified are used to obtain a Benefit-Cost Ratio (BCR) calculated at the household level. The calculated BCR for the agricultural insurance programme averaged for the sample insured households was 2.0, which indicates that the programme had a positive impact, and the overall benefits outweighed the costs.

3.2. The Philippines

Table 2 shows the summary of the BCR. With catastrophic events assumed to occur annually, the net present value (NPV) for a 10-year period at 15% discount rate was about PHP 110,375 per ha (USD 2155) and PHP 62,925 per ha (USD 1229) for rice production with and without crop insurance, respectively. The corresponding BCR was found to be 1.49 for insured farms and 1.31 for uninsured ones. These results suggest that in the case where catastrophic events occurred annually, rice production without crop insurance is still financially profitable as can be seen from NPV greater than zero and BCR greater than 1. However, availing insurance increases the ratio further. Availing of crop insurance can increase the financial profitability of rice production since farmers with insurance have higher NPV and BCR compared with farmers without insurance. Overall, there is an incentive to avail crop insurance given that the difference between the NPV of insured and uninsured (PHP 47,450 or USD 927) is quite significant. In addition, the premium paid in present value terms (PHP 22,244 or USD 424) is only about 32% of the payout received (PHP 69,694 or USD 1361).

| Scenario | BCR |

| With catastrophic events every year | 1.49 |

| With catastrophic events based on actual data | 1.32 |

| Without catastrophic events | 1.18 |

TABLE 2. Summary of benefit-cost analysis results in the Philippines.

A similar trend has been observed in the scenario with catastrophic events based on actual data. With catastrophic events occurring at 60% probability (6 out of 10 years), the NPV of insured farms have reduced to PHP 72,956 per ha (USD 1425) and the BCR to 1.32. Nonetheless, these are still higher than uninsured farms with NPV of PHP 62,925 per ha (USD 1229) and BCR of 1.31. Overall, it is still financially attractive to avail crop insurance since premiums paid in present value terms are also relatively smaller than the payout received by the farmers.

In the scenario without catastrophic events, rice production for both insured and uninsured farmers was still profitable but this time uninsured farms have realized a higher benefit than those who availed of crop insurance. It is, therefore, not financially attractive to avail of crop insurance when catastrophic events are not realized at certainty in any year since farmers will just incur additional costs of premium payment for the insurance coverage without receiving any compensation at all. This implies that crop insurance is only useful when catastrophic climate events are known with certainty. Since catastrophic events are not predictable, it is suggested that crop insurance may need to be obtained every year.

3.3. Malaysia

In Malaysia, the study focused on house insurance against floods. Contrary to expectation, this study did not find evidence of significant difference between insured and uninsured in terms of the number of lost working days, household adjustment on consumption, amount spent for repairing a damaged house, willingness to invest in DRR efforts and economic status 6 months after a flood occurrence.

Table 3 provides the estimated benefits and costs of flood insurance for a community. The data is based on a 3-year interval of a flood event. None of the respondents incurred interest charges due to borrowing thus the value is nil. Only two respondents indicated that they had to borrow, the need to borrow is minimal as the district office has allocated sufficient support (food and shelter) during and after the flood occurrence. Only one respondent indicated using the insurance payout for house improvements (increased precautionary measures).

TABLE 3. Estimated benefits and costs of insurance to households.

A number of respondents indicated that they used all the insurance pay-out for house repairs and that only a partial amount of the compensation was used for repair cost. The respondents were unwilling to spend full repair cost due to the anticipation that they may face future flood damages.

Although respondents have received compensation for the flood losses, none indicated that they have recovered fully. Nonetheless, all respondents assert that insurance is an important tool to help them to recover from losses due to flood. The majority of respondents did not feel that the money invested in insurance premiums can be used for more gainful livelihood activities and they indicated their intention to renew the insurance policy.

4. Conclusions

This paper presented the benefits and costs accrued from insurance in a study carried out in India, the Philippines and Malaysia using household surveys among the insured populations. The findings discussed in this paper suggest that insurance may assist communities to recover and may positively influence disaster risk reduction, as the estimated benefits of insurance outweigh the estimated cost. The positive BCR indicated that, overall, crop insurance was successful as an economic tool. However, as a large proportion of the variables could not be quantified into monetary values due to lack of sufficient data, the BCR does not portray a complete encompassing value of benefits and costs.

Results indicate that insurance helped communities to make additional investments when compared to the uninsured indicating the positive impact on the savings of the insured. Insurance also avoided distress sale of assets. However, insurance did not completely stop the insured from taking loans to cover the losses. This indicates that insurance payouts were not sufficient to cover losses accrued from disasters. In addition, instances were seen where the insured had to make consumption adjustments during disaster years akin to that of the uninsured indicating that the insurance was not able to smooth the income fluctuations. Despite the subsidized premiums, insurance premiums were felt to be costly by most of the insured and delayed payouts have stressed the insured especially in India where payouts were reported to be delayed as late as 7 months. Insurance can increase the NPV, compared to the uninsured, and makes economic sense to invest.

From the results presented in this study, it is evident that the higher benefits compared to costs accrued to the insurance subscribers provides an impetuous for further promoting insurance in the case study countries in specific and in the Asia region in general. Subsidizing the premiums has certainly played an important role especially in making insurance accessible, even though some of the respondents felt the insurance premiums costly even after subsidy. In addition, subsidized premiums have played a significant role in keeping the positive BCR.

The results presented in this paper should be interpreted keeping in view the following limitations. The cost of ineffective implementation of the insurance programme, particularly the long period between loss and payment of claims, could not be included in the BCR. Insurance has demonstrated particular proficiency in assisting farmers with short-term coping, however, this has been hindered by inefficient payout delivery systems. Delayed payments are a significant cost that also has the potential to diminish the beneficial impacts of insurance, particularly the loss coping benefits. In the absence of timely payouts, farmers will turn to informal and unsustainable coping strategies, such as loans from money lenders and sale of productive assets. This can be aggravated when farmers make decisions based on the security provided by insurance; uncompensated and delayed payments can lead to an income shock to the household. Uncompensated losses due to basis risk in yield-based insurance or due to uncovered losses is a significant impediment to farmers’ confidence in insurance.

Significant long-term impacts of insurance on farmers’ livelihoods in the region have yet to be materialized; changes in farmer behaviour relating to confidence building and associated positive impacts on farm management practices are yet to be realized, and significant impacts on profits and assets are only slowly emerging. In India, 90% of farmers said that there was very low potential for implementing alternatives to crop insurance. Primary drivers for the uptake and preference for insurance are its mandatory linkage to crop loans and subsidies on premiums. Nearly all the insured farmers stated that accessing credit from banks was the primary reason they had taken crop insurance, especially in India.

Dissemination of knowledge regarding on-farm risk management strategies could be useful to strengthen risk management capacities of farmers. In conclusion, although theoretically the benefits clearly outweigh the costs, further efforts are required to completely realize the potential of insurance. Based on responses given by the respondents, it is recommended that corrective measures should be done by the government and insurance providers to improve insurance programmes particularly on its delivery system and the payout amount.

Acknowledgement

The authors gratefully acknowledge the financial support received from APN in implementing this project in the form of funding to the ARCP2014-08CMY-Prabhakar. The authors also would like to thank the various researchers, government staff, NGOs, insurance companies and local communities who participated in the consultations and questionnaire surveys organized as a part of the project.

References

- Clarke, D. J., Clarke, D., Mahul, O., Rao, K. N., and Verma, N. (2012). Weather-based crop insurance in India. World Bank Policy Research Working Paper (5985). Washington D.C., USA: The World Bank.

- Ghosh, N., and Yadav, S. S. (2008). Problems and Prospects of Crop Insurance: Reviewing Agricultural Risk and NAIS in India. Institute of Economic Growth of Delhi Enclave North Campus, Delhi: http://www.iegindia.org/ardl/2008_Crop%20Insurance%20Report_Nilabja.pdf

- Hazell, P. B. (1992). The appropriate role of agricultural insurance in developing countries. Journal of International Development, 4(6): 567-581.

- Hazell, P. B., Pomareda, C., and Valdes, A. (1986). Crop insurance for agricultural development: Issues and experience. Biblioteca, Venezuela: IICA.

- Mechler, R. (2005). Cost-benefit analysis of natural disaster management in developing countries. GIZ and Federal Ministry of Economic Cooperation and Development.

- Mechler, R. (2016). Reviewing estimates of the economic efficiency of disaster risk management: opportunities and limitations of using risk-based cost–benefit analysis. Natural Hazards, 81(3): 2121-2147.

- Mechler, R., Hochrainer, S., Kull, D., Singh, P., Chopde, S., Wajih, S., and The Risk to Resilience Study Team. (2008). Uttar Pradesh drought cost-benefit analysis, India (Risk to Resilience Working Paper No. 5). M. Moench, E. Caspari, and A. Pokhrel (Eds.). Kathmandu, Nepal: Institute for Social and Environmental Transition-Boulder, Institute for Social and Environmental Transition-Nepal, and Prevention Consortium.

- Mishra, P. K. (1994). Crop insurance and crop credit: Impact of the comprehensive crop insurance scheme on cooperative credit in Gujarat. Journal of International Development, 6(5): 529-567.

- Prabhakar, S.V.R.K., Rao, G. S., Fukuda, K., and Hayashi, H. (2013). Promoting risk insurance in the Asia-Pacific region: Lessons from the ground for the future climate region under UNFCCC. In: P. Schmidt-Thome and J. Knieling (Eds.), Implementing Climate Change Adaptation Strategies. UK, London: Blackwell Publishers, pp 327.

- Prabhakar, S.V.R.K., Pereira, J.J., Pulhin, J.M., Rao, G.S., Scheyvens, H. and Cummins, J. (Eds.) (2015). Effectiveness of Insurance for Disaster Risk Reduction and Climate Change Adaptation: Challenges and Opportunities. IGES Research Report No 2014-04. Hayama, Japan: Institute for Global Environmental Strategies.

- Rosenzweig, M. R., and Stark, O. (1989). Consumption smoothing, migration, and marriage: Evidence from rural India. The Journal of Political Economy, 97(4): 905-926.

- Rosenzweig, M. R., and Wolpin, K. I. (1993). Credit market constraints, consumption smoothing, and the accumulation of durable production assets in low-income countries: Investments in bullocks in India. Journal of Political Economy, 97: 223-244.

- Townsend, R. M. (1994). Risk and insurance in village India. Econometrica: Journal of the Econometric Society, 62: 539-591.

- Venkatesh, M. (2008). Crop insurance in India: A study. Journal of the Insurance Institute of India, 6(1): 15-17.